Investment Assessment

Tegoprubart: a CNI-free bet on tolerability in kidney transplant

Investment assessment of Tegoprubart (Eledon Pharmaceuticals, NASDAQ: ELDN). As of June 21, 2026. Informational only, not investment advice.

Tegoprubart's Phase 2 missed its primary endpoint, and the Street rates the stock Strong Buy. Both are true, and their coexistence is the thesis. The trial was never built to win on efficacy. It was built to win on tolerability, and on that axis it separated cleanly from the standard of care.

What BESTOW showed

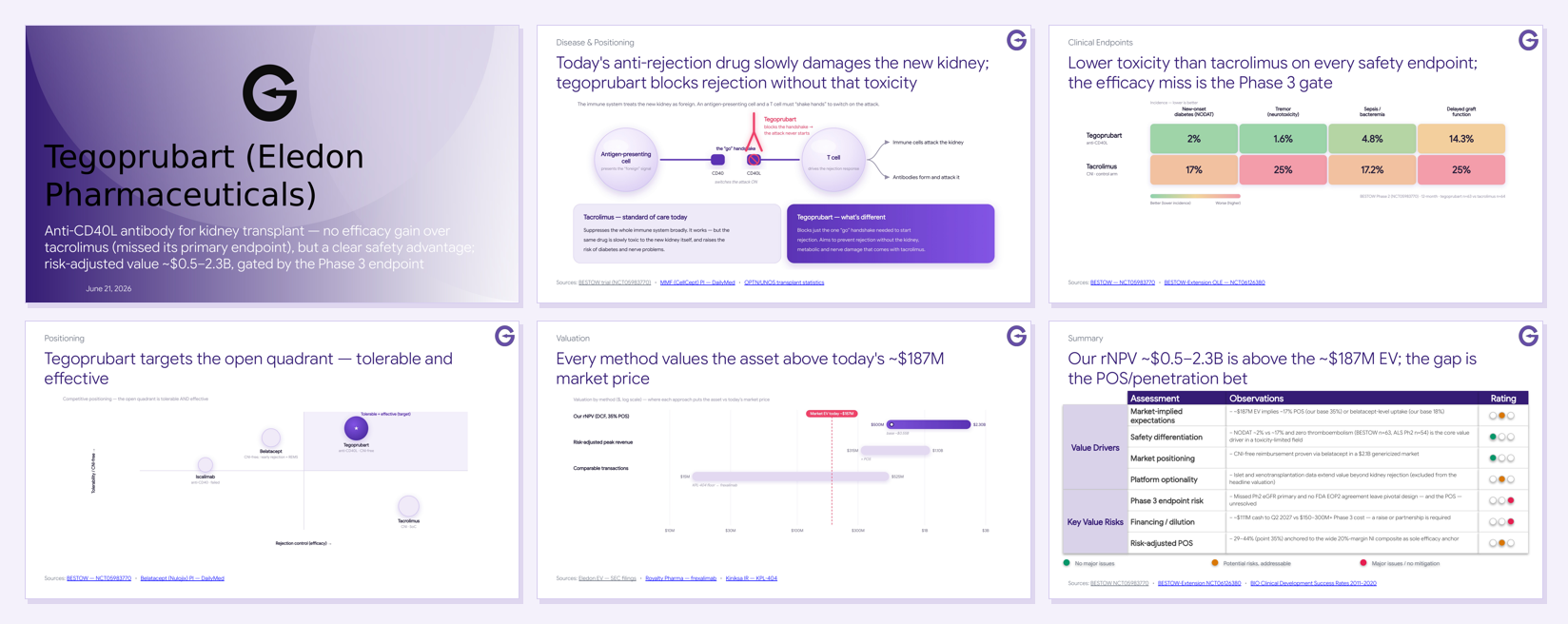

Tegoprubart is a humanized, Fc-silenced anti-CD40L (anti-CD154) monoclonal antibody developed by Eledon Pharmaceuticals for the prevention of rejection in kidney transplant. Its pivotal-readiness rests on the BESTOW Phase 2 trial, a randomized, head-to-head comparison against tacrolimus, the calcineurin inhibitor (CNI) that has anchored maintenance immunosuppression since 1994.

In BESTOW, tegoprubart did not clear its primary efficacy endpoint. Mean 12-month eGFR was 69 vs 66 mL/min/1.73m² against tacrolimus, not statistically significant. A non-inferiority composite (death / graft loss / biopsy-proven rejection / loss-to-follow-up) was met, but within a wide 20-point margin. On a pure efficacy read, that is a miss.

The thesis was never efficacy. It is tolerability.

Why a missed endpoint still matters

Tacrolimus works, but the same drug that controls rejection is slowly toxic to the very organ it is meant to protect. Chronic CNI exposure drives nephrotoxicity, new-onset diabetes (NODAT), and neurotoxicity, and that cumulative injury is a leading cause of late graft loss. The unmet need in kidney transplant is not another drug that controls rejection at the cost of the graft; it is a tolerable, CNI-free maintenance backbone. Today the only approved CNI-free option, belatacept, is capped by higher early rejection and an EBV-seronegative PTLD boxed warning.

Tegoprubart attacks the problem one step upstream. Rejection requires a costimulatory "handshake" between an antigen-presenting cell and a T cell; tegoprubart blocks the CD40–CD40L arm of that handshake, switching off the activation signal without the broad, organ-toxic suppression of a CNI.

The data wins on safety

This is the heart of the case. Against tacrolimus in BESTOW, tegoprubart's safety separation is large and consistent across every measured tolerability dimension.

| Safety endpoint | Tegoprubart | Tacrolimus |

|---|---|---|

| New-onset diabetes (NODAT) | ~2% | ~17% |

| Tremor (neurotoxicity) | 1.6% | 25% |

| Sepsis / bacteremia | 4.8% | 17.2% |

| Delayed graft function | 14.3% | 25% |

These are not marginal differences. A CNI-free regimen that removes the diabetes, neurological, and infection burden of tacrolimus, delivered as a guaranteed infusion (no oral-adherence risk, reimbursed under Medicare Part B), addresses the exact failure mode that limits the standard of care.

The decisive question is regulatory. Will the FDA let a CNI-free maintenance agent win on the toxicity it removes rather than on an eGFR number it did not beat?

Full deck

Full deckFull presentation

See the full Tegoprubart deck

We’ll email you the link to the full slide deck.

Positioning

Every other agent in the field trades one axis for the other. Tacrolimus is effective but toxic. Belatacept is CNI-free but carries higher early rejection and a PTLD REMS. The prior anti-CD40 antibodies (iscalimab, bleselumab) stalled. Tegoprubart's Fc-silenced, ligand-side design is aimed squarely at the open quadrant.

The valuation gap is the trade

At a ~$187M enterprise value, the market is pricing tegoprubart at roughly 17% probability of success, or belatacept-level uptake at a higher probability. Our risk-adjusted NPV, built as a proper DCF (net peak revenue × multiple × probability of success, less the risk-borne Phase 3 spend), lands at ~$0.5–2.3B with a base case near $0.55B at 35% POS. Comparable CD40/CD40L transactions span an early-M&A floor (KPL-404, ~$15–18M) to a de-risked royalty (frexalimab, $525M).

An rNPV above the EV is not a claim that the stock is cheap. It is a claim that the market is pricing a lower probability of success than we are. Read in reverse, the ~$187M EV implies the market's odds, and the upcoming catalysts adjudicate the difference.

The catalysts

Two near-term events fix the Phase 3 endpoint design, and with it the probability of success the whole valuation turns on:

- FDA End-of-Phase-2 meeting (2026). Whether the agency accepts a tolerability-anchored or tighter non-inferiority design is the single largest value inflection. A favorable signal re-rates POS toward 45%+.

- BESTOW-Extension open-label readout (expected mid-2026). The 18–24-month eGFR trajectory and stable rejection are the durability signals that move the bear case toward base.

The caveats

- Efficacy is unproven, not just unshown. Biopsy-proven rejection ran numerically higher than tacrolimus (20.6% vs 14.1%). The pivotal must lock in a tighter margin or a tolerability co-primary; the unreleased 95% CI on the primary contrast matters.

- Financing. ~$111M cash runs to Q2 2027 against a $150–300M+ Phase 3. A raise or partnership is required, a near-term dilution-or-deal catalyst in its own right.

- Class history. Both prior anti-CD40 agents failed in transplant on acute rejection. The target's tolerability is validated; its efficacy at pivotal scale is not.

This is an endpoint-and-financing bet, not a clean efficacy win.

Assessment

Tegoprubart is the rare asset where the miss is the opportunity. The market has priced the efficacy disappointment; it has been slower to price the tolerability profile that defines the unmet need in a CNI-toxicity-limited field. The FDA End-of-Phase-2 outcome and the BESTOW-Extension readout are what convert that gap into either a re-rating or a confirmation of the market's skepticism. Composition-of-matter protection runs to 2036 with an effective loss of exclusivity around 2041–2043, leaving room for the value to be realized if the science holds.

Key sources

- BESTOW Phase 2 — NCT05983770 · BESTOW-Extension OLE — NCT06126380 · Phase 1b CNI-free — NCT05027906

- Standard of care: Belatacept (Nulojix) label — DailyMed · Mycophenolate (CellCept) label — DailyMed · NICE TA481 — immunosuppressive therapy for kidney transplant

- Market & data: OPTN national kidney data · SRTR Annual Data Report — Kidney · BIO Clinical Development Success Rates 2011–2020

- Comparables: Royalty Pharma — frexalimab royalty · Eledon SEC filings (EDGAR)